Before allowing a third party to perform work on the association's common areas (plumbing, electrical, roofing, painting, street paving, landscaping, etc.), associations must make sure the contractor is licensed and has the following insurance:

- Workers Compensation. Workers' compensation policies protect injured workers.

- Commercial General Liability (CGL). CGL policies protect against lawsuits that may result from bodily injury or property damage arising from the contractor's work. The policy should include an endorsement naming the association as "Additional Insured" which provides additional protection to the association. However, such protections can be voided if the policy excludes coverage for multi-family developments (see "Exclusions" below).

-

Completed Operations. This covers any damages that may arise after the work is completed. For example, if a new roof were to leak at some point after it was completed and damaged the common areas and an owner's unit, a claim can be tendered to the roofer's insurance company.

-

Errors & Omissions. Architects and engineers who prepare specifications for contractors or who consult with the association should carry E&O professional liability insurance. E&) insurance covers mistakes made by professionals.

Proof of Insurance. All contractors/vendors who work for an association should be required to provide the board with proof of insurance prior to the commencement of work.

Condominium Exclusion. Perhaps the most important item to look for when reviewing a vendor's insurance is whether it has a "Multi-Family" or "Multi-Unit" exclusion in the insurance policy. If they do, they are essentially UNINSURED if they perform any work for a condominium association. If that is the case, DO NOT hire the vendor.

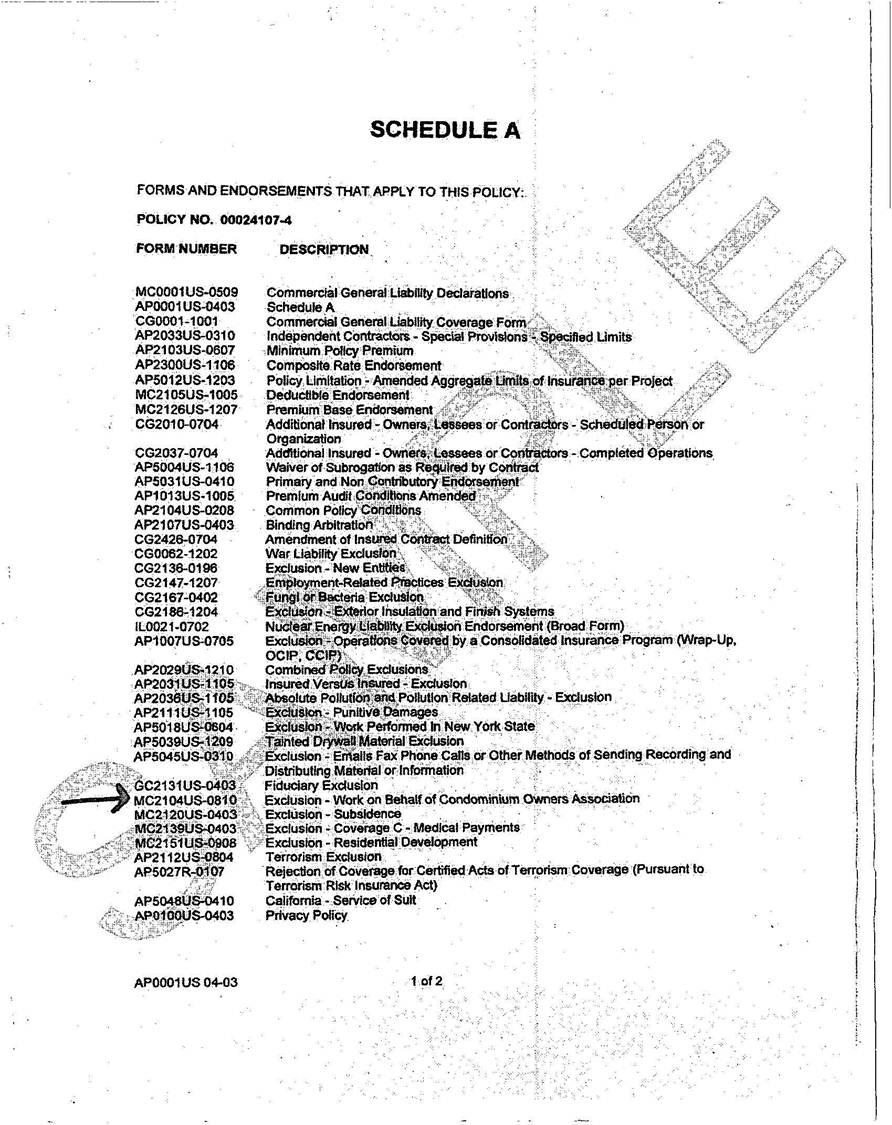

Some policies are more explicit and will specifically exclude coverage for any work done by a vendor for a condominium association. See the example below.

Locating Exclusions. Because exclusions are typically not listed on the certificate of insurance given to the association, boards and managers must request a complete copy of the contractor’s CGL policy and have the association's insurance broker or attorney review it.

ASSISTANCE: Associations needing legal assistance can contact us. To stay current with issues affecting community associations, subscribe to the Davis-Stirling Newsletter.