Bank Foreclosures on HOA Units

Mortgage in First Position. A purchase money lien (mortgage) is recorded when a buyer borrows money to purchase a property. A mortgage secures the lender's debt. Because purchase money liens are always first in line, they have priority over all other liens. If the association forecloses, it takes ownership subject to any liens recorded before the association's assessment lien.

Mortgage in First Position. A purchase money lien (mortgage) is recorded when a buyer borrows money to purchase a property. A mortgage secures the lender's debt. Because purchase money liens are always first in line, they have priority over all other liens. If the association forecloses, it takes ownership subject to any liens recorded before the association's assessment lien.

Assessment Liens. Liens recorded by an association against a property for delinquent assessments are behind or "junior" to any other liens recorded on the property. Because of their junior status, an assessment lien is wiped out if the lender forecloses on the owner. (Streiff v. Darlington (1937) 9 Cal.2d 42) When this happens, the debt owed to the association remains collectible but is no longer secured by the property. The association must obtain a money judgment against the delinquent party in small claims or superior court to collect the delinquent assessments.

Debt of the Owner. An assessment becomes an owner's debt when the association levies it. However, the debt is a homeowner's personal obligation until the association records a notice of delinquent assessment against his/her interest in the development. Recording a notice creates a lien and gives the association a security interest in the lot or unit against which the assessment was imposed—the lien dates from the time the lien is recorded. California follows the "first in time, first in right" system of lien priorities. Condominium assessment liens follow this same system. An assessment lien is before all other liens recorded after the notice of assessment, except that the [CC&Rs] may provide for the subordination thereof to any other liens and encumbrances. (Diamond Heights v. Financial Freedom, internal cites and quotes deleted)

Bank Foreclosure. Whenever a lender forecloses on an owner, the association's collection efforts are hampered because lenders often fail to notify the association of the new owner's name and address (whether it be a third party or the bank itself). If there is no third-party purchaser at a bank's foreclosure auction, the property goes into the bank's REO (Real Estate Owned) Department, which could be in another state, further complicating an association's collection efforts. If the bank forecloses on the mortgage and takes ownership of the property, the association no longer has a claim on the property for the delinquent assessments. The association still has the right to sue the owner for a money judgment.

Request for Notice. Effective January 1, 2009, lenders must notify associations whenever they foreclose on property in an association. The trustee must mail the deed within 15 business days of the sale. (Civ. Code § 2924b(f)(1)) Effective January 1, 2010, associations may record a blanket "Request for Notice" that requires a trustee to mail a copy of the trustee's deed to the association once a foreclosure sale takes place. (Civ. Code § 2924b) It must contain (i) a legal description or assessor's parcel number of all units/lots in the development, (ii) the name and address of the association or managing agent, and (iii) a statement that the association was created to manage a common interest development. To avoid their notice requirements under the above statute, many banks foreclosed on properties and refused to record the transfer of ownership. It allowed them to avoid paying homeowner association assessments because they believed their duty to pay did not begin until they recorded the deed. Effective January 1, 2013, lenders must record foreclosure sales within 30 days of the sale date. (Civ. Code § 2924.1)

Judicial Foreclosure

Benefits. The primary benefit of a judicial foreclosure over a nonjudicial foreclosure (trustee sale) is the ability to obtain a personal money judgment in addition to the foreclosure. This feature is relevant if the property's equity is insufficient to cover the association's lien once all liens senior to the association's lien have been satisfied. It also allows for the court-authorized publication of specific notices when the owner is deceased.

Initiating Judicial Foreclosure. Judicial foreclosure procedures are outlined in Civil Code § 5660. It starts with sending a notice of intention to lien (a pre-lien letter), followed by recording a notice of assessment lien. The Association then files a lawsuit seeking two remedies: (i) money damages against the owner personally and (ii) the right to foreclose on the association’s lien.

Litigation. In approximately 95% of judicial foreclosure cases, a defendant fails to answer the complaint, which permits the Association to file a default against the defendant. The legal effect of a default is to remove the defendant as an active litigant in the case, which then permits the association to seek a judgment against the defendant. If the defendant answers the lawsuit, the case is litigated as any other case.

Deficiency Judgment. Should the board elect to foreclose on the property and the proceeds from the sale not yield enough to cover the amount of the association’s judgment, the association can apply for a deficiency judgment against the defendant. The application for a deficiency judgment must be filed within three months of the issuance of the foreclosure sale. Failure to seek a deficiency judgment within this time waives the Association’s right to pursue it later, without exception. (Code Civ. Proc. § 726; Life Savings Bank v. Wilhelm (2000) 84 Cal.App.4th 174) A deficiency judgment is effectively a hearing before the court for the court to determine the amount of deficiency based on the fair market value of the property sold.

Excess Funds. If the property has more equity than what is needed to cover the judgment amount, the former owner has a right to recover any surplus funds after the costs of sale have been paid, the judgment is paid, and any senior and then junior liens are satisfied (in order of their priority) (Cockerell v. Title Ins. & Trust Co. (1954) 42 Cal.2s 284; Schumacher v. Gaines (1971) 18 Cal. App.3d 994)

Redemption Rights. One of the negatives of judicial foreclosures is the owner's right of redemption. In a trustee's sale, the redemption period is 90 days. In a judicial foreclosure, the redemption period is 90 days if the sale proceeds are sufficient to satisfy the association's lien. (Code Civ. Proc. § 729.030(a)) The redemption period becomes one year if the monies from the sale are insufficient to satisfy the delinquency plus interest and collection costs. (Code Civ. Proc. § 729.030(b)) The redemption period prevents the association from taking possession of the property unless the foreclosed owner voluntarily turns over possession.

Negatives. Judicial foreclosures can take longer and cost more than a simple money judgment or a trustee's sale, especially when the delinquent owner contests the matter. As a result, associations tend to use small claims and superior court personal money judgments and trustee sales more often than judicial foreclosures.

Nonjudicial Foreclosure (Trustee Sale)

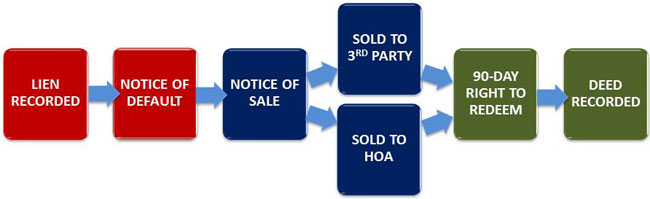

Delinquent Owners. If an owner becomes delinquent in the payment of their assessments, whether regular or special, totaling $1,800 or any amount over twelve months delinquent, an association can foreclose on and sell the owner's property. The following is the sequence of the foreclosure process.

| Boards must approve and then record a lien to protect the association's interest. |

A notice of default starts the foreclosure process once the board approves the sale. |

A notice of sale sets the date for auctioning the property. |

Auction of the property is done by a trustee. Sale defaults to the HOA if no bid exceeds the delinquency amount. |

Upon sale, a 90-day redemption period starts. |

The foreclosure timeline is approximately one year.

|

| Foreclosure Timeline. Some dates on the timeline may vary depending on circumstances. |

| Day 1 |

Assessments are due (usually the 1st day of the month). |

| 16 |

A late fee of 10% or $10.00, whichever is greater (unless CC&Rs specify a smaller amount), may be levied 15 days after assessments are due. (Civ. Code § 5650(b)(2)) However, the 15-day period may be longer if an association's governing documents specify. |

| 30 |

The association may charge interest at 12% per annum (unless the CC&Rs set a lower rate). (Civ. Code § 5650(b)(3)) |

| 46 |

Pre-lien letter with a copy of the association's assessment collection policy and notice of owner's right to meet and confer (IDR). (Civ. Code § 5660(e); Civ. Code § 5670)) |

| 76 |

Record lien against the property (Notice of Delinquent Assessment) and give notice of right to IDR or ADR. (Civ. Code § 5705(b)) |

| 107 |

Notice of Default and Election to Sell. (This step initiates the foreclosure.) |

| 218 |

Sale of the Unit and the start of the 90-day redemption period. |

| 308 |

The owner's redemption rights terminate. |

Pre-Lien Letter

At least thirty (30) days before recording an assessment lien on an owner’s separate interest for delinquent assessments, late charges, interest, collection fees, and costs owed by that owner to the association, the association is required to provide the owner with a pre-lien letter (aka “intent to lien letter,” “pre-lien notice,” etc.) by certified mail. (Civ. Code § 5660)

Required Information. The pre-lien letter must be sent to the owner of record via certified mail and include all of the following information:

- Description of Collection/Lien Enforcement Procedures. A general description of the collection and enforcement procedures of the association (the association’s assessment collection policy). (Civ. Code § 5660(a))

- Debt Calculation Method. A general description of the calculation method of the delinquent amount owed to the association. (Civ. Code § 5660(a))

- Right to Inspect Records. A statement that the owner has the right to inspect the association’s records under Civil Code Section 5205. (Civ. Code § 5660(a))

- Required Foreclosure Notice. The following statement in 14-point boldface type, if printed, or in capital letters, if typed: “IMPORTANT NOTICE: IF YOUR SEPARATE INTEREST IS PLACED IN FORECLOSURE BECAUSE YOU ARE BEHIND IN YOUR ASSESSMENTS, IT MAY BE SOLD WITHOUT COURT ACTION.” (Civ. Code § 5660(a))

- Itemized Statement of Debt. An itemized statement of the charges owed by the owner, including items on the statement that indicate the amount of any delinquent assessments, the collection fees and costs, reasonable attorney’s fees, and any late charges and interest, if any. (Civ. Code § 5660(b))

- Non-Liability for Association’s Error. A statement that the owner shall not be liable to pay the late charges, interest, collection fees, and costs if the assessment was paid on time to the association. (Civ. Code § 5660(c))

- Right to Request a Meeting to Discuss the Payment Plan. The owner’s right to request a meeting with the board to discuss a payment plan, as provided in Civil Code Section 5665. (Civ. Code § 5660(d))

- Right to Request IDR. The owner’s right to dispute the assessment debt by submitting a written request for dispute resolution to the association under the association’s “meet and confer” program established under Civil Code Section 5900 et seq. (Civ. Code § 5660(e)) If the owner requests IDR before the lien is recorded, the association must participate in IDR with the owner before recording the lien.

- Right to Request ADR. The owner’s right to request alternative dispute resolution (ADR) with a neutral third party under Civil Code Section 5925 et seq. before the association may initiate foreclosure against the owner’s separate interest, except that binding arbitration shall not be available if the association intends to initiate a judicial foreclosure. (Civ. Code § 5660(f))

For delinquencies less than $1,800, some associations collect the assessment, late fees, interest, and collection costs by filing a small claims action. (Civ. Code § 5720(b)(1))

Multiple Owners. Whenever multiple owners on title live at different addresses, notice must be given to all owners at each address. This can be done in one letter with multiple addressees and addresses (all owners on title at all addresses) at the top, and then mailed to everyone. Any additional expenses can be included in the HOA's collection costs.

Certified Mail Required

Although Civil Code § 2924b(b) requires that notices be sent by registered or certified mail, it does not require a signed receipt before an association moves to the next step in the foreclosure process.

Refusal to Sign. To require a signed receipt means a person could stop foreclosure by refusing to sign for the letters. Because owners often refuse to sign for certified mail, Civil Code § 2924b(e) also requires that notice be given concurrently by first-class mail. The court in Bear Creek v. Edwards addressed the issue of unsigned receipts and determined that notice cannot be defeated by a person's willful failure to accept certified mail. The court commented that,

...while a signed return receipt may create a rebuttable presumption that the notice was received, the absence of such a signed return receipt does not negate any other presumptions concerning mailed items. Under Evidence Code section 641, "[a] letter correctly addressed and properly mailed is presumed to have been received in the ordinary course of mail."

Notice Requirements. A foreclosure starts with a Notice of Default (NOD). After three months, a Notice of Sale can be prepared. For the NOD, there is an additional requirement of personal or substituted service for assessment lien foreclosures as outlined in Civil Code § 5710(b). Service of the NOD can be a problem when the owner cannot be located or is deceased. As for a Notice of Sale, it must be recorded, published, mailed, and posted, but not personally served.

Foreign Countries. According to the US Postal Service website, an association can send First Class International mail and add a Certificate of Mailing. While technically different than Certified Mail, the certificate provides evidence that you sent the notice. Since the return receipt feature and proof of delivery are not required by Civil Code § 5660, the important feature in both Certified Mail and Certificate of Mailing is proof of mailing. Registered Mail is also available with First-Class International mail, but it is more expensive. Although the primary purpose of registered mail is to insure valuables, it also provides proof of mailing. Therefore, both the Certificate of Mailing and Registered Mail options should be acceptable substitutes for Certified Mail when sending a pre-lien notice to someone in another country.

Board Resolution to Lien

The decision to record a lien for delinquent assessments must be made by the board by a majority vote in an open meeting and recorded in the minutes of that meeting before recording the lien. (Civ. Code § 5673) This can be done by a simple motion or by a formal resolution. The statute does not explicitly state that associations must keep owners' names confidential. However, the best practice is to keep them confidential. Following is a sample resolution:

WHEREAS, Section 5673 of the Civil Code requires the board of directors to authorize, in an open meeting, the recording of liens against the separate interests of owners with delinquent assessments;

WHEREAS, on {date of pre-lien letter}, more than thirty (30) days before this meeting, the Association sent a certified letter to the Owner of:

Account No. _____________________

Under Section 5660 of the Civil Code, the letter contained a notice of delinquent assessment, which included but was not limited to describing the Association's collection and lien enforcement procedures, an itemized statement of charges, the owner's inspection rights, the owner's "meet and confer" rights, and the owner's ADR rights.

WHEREAS, Owner remains delinquent in the payment of their assessments, exclusive of late fees, interest charges, and other collection-related amounts;

RESOLVED, the Association authorizes {entity assigned to handle lien} to place a lien on this property for the delinquent amounts and any late fees, interest charges, and other collection-related amounts.

The board of directors adopted this resolution at an open meeting held on the ____ day of ___________, 20____.

__________________________________

Signature of Authorized Board Member

Title: _____________________________

|

Errors in Liens. If it is determined that a lien previously recorded against the separate interest was recorded in error, the party who recorded the lien shall, within 21 calendar days, record or cause to be recorded in the office of the county recorder in which the notice of delinquent assessment is recorded a lien release or notice of rescission and provide the owner of the separate interest with a declaration that the lien filing or recording was in error and a copy of the lien release or notice of rescission. (Civ. Code § 5685(b))

Board Authorization to Foreclose

Associations can record a lien but may not foreclose until the delinquent assessment is at least $1,800, or the delinquency is at least twelve months old. (Civ. Code § 5720(b)(2))

Executive Session Vote. The board must decide whether to initiate foreclosure. They cannot delegate the decision to an agent of the association. The board must approve the decision by a majority vote of the directors in executive session. (Civ. Code § 5705(c))

Open Meeting Minutes. The vote must then be recorded in the minutes of the next open meeting of the board. However, boards must maintain the confidentiality of owners' names by identifying properties by the assessor's parcel number rather than by the owner's name. A board vote to approve a lien's foreclosure must occur at least thirty days before any public sale. (Civ. Code § 5705(c)) Failure to do so could be the basis for a legal challenge to the foreclosure action.

WHEREAS, the Association previously recorded, under Section 5673 of the Civil Code, a lien against parcel number _____________________ for delinquent assessments;

WHEREAS, Section 5705 of the Civil Code requires the board of directors to authorize, by majority vote of the board in executive session, the foreclosure of a lien for delinquent assessments;

WHEREAS, the Owner is now delinquent in the payment of regular or special assessments [OPTION 1] in an amount that equals or exceeds one thousand eight hundred dollars ($1,800), exclusive of any accelerated assessments, late charges, fees, and costs of collection, attorney's fees, or interest [OPTION 2] which are more than twelve months delinquent;

RESOLVED, the Association authorizes {entity assigned to handle foreclosure} to foreclose on the lien to recover the delinquent amounts and any late fees, interest charges, and other collection-related amounts.

The board of directors adopted this resolution at an executive session held on the ____ day of ___________, 20____.

__________________________________

Signature of Authorized Board Member

Title: ____________________

|

Recording a Notice of Default

One of the procedural requirements for a nonjudicial foreclosure is the recording of a Notice of Default. (Civ. Code § 2924(a)(1)) The recording of the Notice initiates the foreclosure process. The Notice must include information identifying the property's address, a statement that the owner of the property has breached their obligation to pay assessments to the association, and a statement of the association’s information and its election to sell the property. (Civ. Code § 2924(a)(1)) Civil Code § 2924c(b) requires the following:

- The potential for the property to be sold without court action,

- The owner’s right to halt the nonjudicial foreclosure action by paying the amounts owed, and

- The owner may lose legal rights if they do not take prompt action. (Civ. Code § 2924c(b))

Serve of Notice of Default. In addition to serving the Notice of Default on the owner, it must be mailed to persons with a legal interest in the property or the right to be provided with a copy of the Notice of Default. (Civ. Code § 2924b(b)-(c))

90-Day Right of Redemption

If the property is sold at auction, the owner has a 90-day right of redemption. It gives the owner the right to re-acquire ownership of their property. This right had previously been associated with judicial foreclosures only. Beginning January 1, 2006, the right was extended to nonjudicial assessment lien foreclosures. If an association sells a property via nonjudicial foreclosure (a trustee's sale), the highest bidder, whether the association or a 3rd party, takes ownership subject to a 90-day right of redemption.

Redemption Price. The redemption period allows the foreclosed owner to "redeem" the property by paying the delinquent amounts plus any collection fees and costs. (Code Civ. Proc. § 729.035, Civ. Code § 5715(b)) If the buyer of the foreclosed property incurs expenses for maintenance and repair work on the unit, which were reasonably necessary for the preservation of the property, he can include those expenses in the redemption price. (Barry v. OC Residential Properties)

Certificate of Sale. During the 90-day redemption period, title to the property does not transfer to the highest bidder. Instead, the trustee records a "certificate of sale," which gives notice of the bidder's right to the property. If the delinquent owner does not redeem the property within the 90-day period, the trustee delivers a Trustee's Deed Upon Sale (TDUS) to the successful bidder, with ownership transferring to the buyer. If the owner exercises the redemption rights by paying all amounts due, a Certificate of Redemption is issued in lieu of a TDUS, and title reverts to the property owner.

Redemption Period Cautions. If the association is the successful bidder on a foreclosed property, the 90-day redemption period limits what it can do until the period ends.

- Eviction. Because the successful bidder does not officially own the property until the end of the redemption period, the bidder has no right of possession and cannot evict the occupant during the redemption period. Once the redemption period ends and the title transfers, the buyer can evict anyone in possession of the property through an unlawful detainer action.

- Damage to Property. If the occupant damages the property, the association cannot enter the property to stop the damage. Instead, it must immediately file a court action to enjoin the occupant from damaging the property. (Code Civ. Proc § 729.090(c))

- Vacant Property. If the property is vacant, the association should secure it and, if personal property is left in it, comply with the storage, notice, and sale of abandoned property laws (Civ. Code § 1980 et seq.) Since the prior owner has the right to redeem the property, the association should not remodel it or rent it out until the redemption period ends and the right of possession transfers to the association.

Right to Rent. The buyer of the foreclosed property has the right to collect rents and profits from persons possessing the property. (Code Civ. Proc. § 729.090(a))

Association Takes Ownership

If there are no bidders at the foreclosure sale, the association takes ownership of the property. At that point, the association can:

- Retain Ownership. This requires making payments on any outstanding senior liens and taxes. This allows the association to put a renter in the property. Whether this is a viable option depends on the economics involved—can the association rent the unit for enough to cover the mortgage payments? In addition, the board needs members to insure the property and pay property taxes.

- Sell the Property. The ability to sell will depend on whether there is any equity in the property since senior liens must be satisfied (unless the lien-holders agree to a short sale).

- Transfer to the Bank. The association can transfer ownership to the senior lienholder via a deed rather than through foreclosure. Whether the bank will accept the deed depends on internal bank policies. Many banks will not accept a deed due to potential title insurance issues. Instead, they prefer to foreclose on the property.

- Allow Bank Foreclosure. Another option is to hold the property but not pay any money to the senior lien holders, allowing them to foreclose on it. If the unit sits empty until the bank forecloses, the association continues to lose the income it would typically receive from a dues-paying owner. A bank foreclosure will not negatively impact the association's credit. The bank's loan is in the prior owner's name, and the bank is foreclosing on the previous owner's mortgage, not the association's. The prior owner's credit is harmed, not the association's. Even if the association's credit were somehow affected, it would have little or no impact. Associations typically do not borrow money to buy consumer goods or property. Typically, they borrow only for major repairs. When that is done, the loan is secured by a special assessment approved by the membership.

Selling HOA-Owned Units

QUESTION: Our HOA foreclosed on a unit last year. The new board decided to sell it without notifying or consulting the membership. Doesn't the board need the membership's permission to sell common property?

ANSWER: A unit or lot acquired through foreclosure does not become common area. The property is identified in the governing documents as a separate interest, not common area. As a result, members do not have the right to enter and use the property as they would common areas. Instead, the property is under the control of the association through its board of directors, who can either rent or sell it without first obtaining membership approval.

Possible Restriction. There might, however, be language in the governing documents restricting the sale of association property over a certain value without membership approval. Depending on the wording of the restriction, it could affect the board's ability to sell it.

ASSISTANCE: Associations needing legal assistance can contact us. To stay current with community association issues, subscribe to the Davis-Stirling Newsletter.